Table of Content

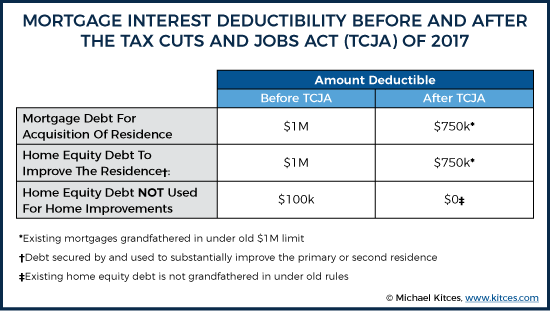

Prior to the Tax Cuts and Jobs Act , you could deduct interest on up to $1 million of home acquisition debt (or $500,000 if you used married-filing-separately status). Home acquisition debt means loans to buy or improve a first or second residence. The rules for deducting home mortgage interest under the new tax law can get complicated. We expect the IRS to issue guidance that will clarify some questions. If you have additional questions or need help substantiating your qualified residence interest deduction, contact your tax advisor. TurboTax estimates that the new tax deduction limitations will push about 90 percent of taxpayers to take the standard deduction, up from about 70 percent in previous years, instead of itemizing their deductions.

Highest rate is applicable to taxable income above $500,000 for single taxpayers and head of household, and $600,000 for married taxpayers filing jointly. So, many taxpayers tapped into their home equity to pay for, say, vacations, college tuition, vehicle purchases and living expenses. And they counted on deducting interest on those loans each tax year. The new rules for deducting interest on home equity loans will put a wrench in those plans, starting in 2018. The good news is not all these changes will apply this upcoming year. On December 2017, President Donald Trump signed the new tax reform law called Tax Cuts and Jobs Act.

For some, interest is still deductible despite the Tax Cuts and Jobs Act

It might even provide some tax benefits since the interest you pay is sometimes deductible. But if you use the money to pay off credit card debt or student loans — or take a vacation — the interest is no longer deductible. But the Internal Revenue Service, saying it was responding to “many questions received from taxpayers and tax professionals,” recently issued an advisory. According to the advisory, the new tax law suspends the deduction for home equity interest from 2018 to 2026 — unless the loan is used to “buy, build or substantially improve” the home that secures the loan. Under prior tax law, a taxpayer could deduct “qualified residence interest” on a loan of up to $1 million secured by a qualified residence, plus interest on a home equity loan up to $100,000.

Also included in this bunch are expenses related to investment fees, legal fees, home office use and alimony for divorces finalized after December 31, 2018. These deductions will be reinstated in 2026 unless Congress votes to extend the current rule. That means it will be a lot tougher to qualify to itemize deductions. If your mortgage existed on Dec. 14, 2017, you’re grandfathered in on the $1 million maximum.

Home Equity Loans and the Cap on Home Loan Tax Deductions

When you sell your primary residence, you can make up to $250,000 in profit if you’re single, or $500,000 if you’re married, and not owe any taxes on those gains. Most people are eligible for this exclusion, but you must have lived in your home for at least two of the five years before you sell. But the re-fi you were planning on using to pay off those credit cards?

H.R.5371). It would make a more lucrative method of determining tax-deductible interest permanent. Be about $20 billion in one year and up to $200 billion over 10 years. Some significant portion of that cash will likely wind up in the pockets of private equity billionaires. Youll receive a Mortgage Interest Statement Form 1098 at the beginning of each year from your lender.If you have deductible home mortgage interest or points reported on Form 1098, then deduct it on your Schedule A , line 8a. Were transparent about how we are able to bring quality content, competitive rates, and useful tools to you by explaining how we make money. Moving Expenses – The deduction for job-related moving expenses has been eliminated, except for certain military personnel.

How Much Does H&r Block Charge To Do Taxes

In response, the IRS recently issued a statement clarifying that the interest on home equity loans, home equity lines of credit and second mortgages will, in many cases, remain deductible. Instead, it is classified as home equity debt; so, you can’t treat the interest on that loan as deductible qualified residence interest for 2018 through 2025. The Tax Cuts and Jobs Act changes the rules for deducting interest on home loans. Most homeowners will be unaffected because favorable grandfather provisions will keep the prior-law rules for home acquisition debt in place for them.

The debt was taken out after December 16, 2017 and was used to buy, build, or improve your home, and the total amount of debt throughout 2019 was $750,000 or less. The debt was taken out after October 13, 1987 but before December 16, 2017 and was used to buy, build, or improve your home, and the total amount of debt throughout 2019 was $1 million or less. Casualty losses for such things as a home burglary or a fire are no longer deductible. To claim a casualty loss, the loss has to fall under a presidentially declared disaster, like a hurricane or earthquake. The little-known fact is that you still deduct home equity loan interest in certain circumstances. Private equity managers also often extract excessive fees from their purchased companies.

Our mission is to protect the rights of individuals and businesses to get the best possible tax resolution with the IRS.

Rebecca Lake is a journalist with 10+ years of experience reporting on personal finance. This copyrighted material may not be republished without express permission. The information presented here is for general educational purposes only.

For taxpayers itemizing deductions on their individual tax return, the mortgage interest deduction and the home equity interest deduction are both still a valuable component of your tax planning. For more information on the mortgage interest or home equity interest deduction, please contact Gloria McDonnell. Historically, borrowers could deduct home equity interest on loans up to $100,000 ($50,000 for married people filing separately).

Note the limitation is per taxpayer which increases the limitation for single co-owners / registered domestic partners. Generally, you have a reasonable basis if your chances of withstanding an IRS challenge are greater than 50%. Reliance on a competent tax advisor greatly improves your odds of obtaining penalty relief. Other possible grounds for relief include computational errors and reliance on an inaccurate W-2, 1099 or other information statement. Tax-filing inaccuracy.These penalties may be imposed, for example, if the IRS finds that your return was prepared negligently or that there’s a substantial understatement of tax.

The same goes if you are taking out a loan and letting the money sit in the bank as your emergency fund. Whats more, the renovations have to be made on the property on which you are taking out the home equity loan. You cannot, for example, take out a loan on your primary residence and use the money to renovate your cottage at the lake. For 2018 through 2025, the new tax law generally allows you to treat interest on up to $750,000 of home acquisition debt as deductible qualified residence interest.

And unlike the deduction for interest on primary mortgages, home equity deductions are disappearing for both new and existing borrowers. In the past, if a taxpayer’s job required certain purchases in order for an employee to perform their job and the employer was unable or unwilling to reimburse the employee, those expenses were tax deductible. For example, employees could deduct mileage driven for work purposes , uniforms, tools, union dues and more as long as they met the 2 percent rule for miscellaneous deductions. BTW, talk with your tax preparer if you prepaid your 2018 property taxes in 2017 in hopes of maxing out your deductions before the tax law change. The rules apply to the return you will file next year, for 2018, said Cari Weston, director of tax practice and ethics for the American Institute of Certified Public Accountants. Interest on home equity loans or lines of credit you paid in 2017 is generally deductible on the return you file this year, regardless of how you used the loan.

No comments:

Post a Comment